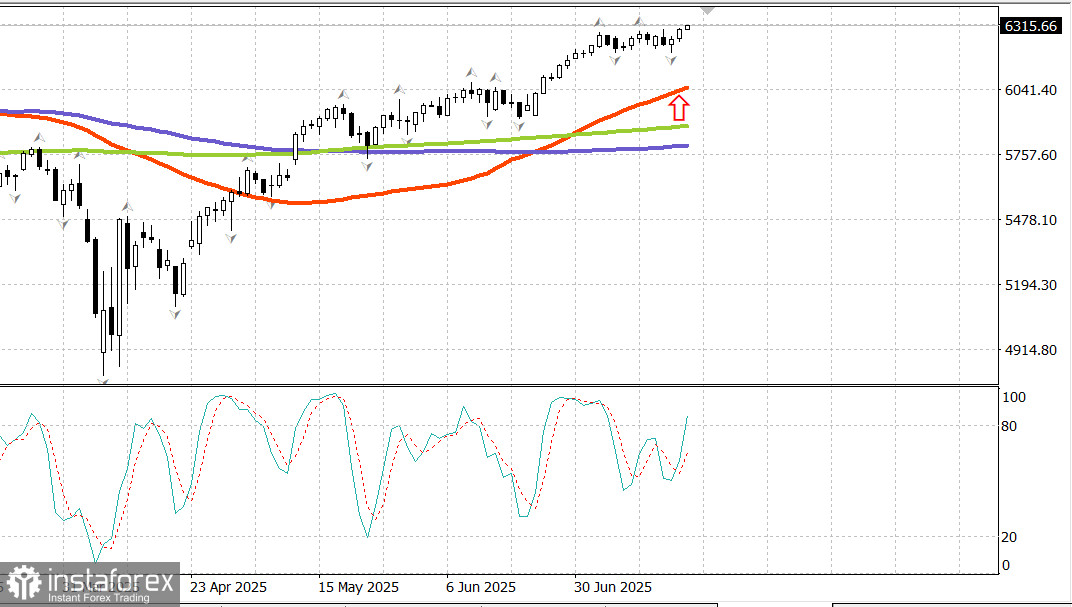

S&P500

Snapshot of major US stock indexes on Thursday

- Dow +0.5%,

- NASDAQ +0.7%,

- S&P 500 +0.5%, S&P 500 closed at 6,297, trading in a range of 5,900 to 6,400.

The stock market was encouraged by some key economic data and earnings reports released before the open, which sparked a broad-based rally, ultimately pushing the S&P 500 (+0.5%) and the Nasdaq Composite (+0.7%) to new all-time highs.

Notable gainers included:

- Travelers (TRV): $261.81, +$9.62 (+3.81%)

- PepsiCo (PEP): $145.44, +$10.09 (+7.5%)

- Citizens Financial Group (CFG): $48.82, +$1.85 (+3.9%)

- Snap-On (SNA): $337.80, +$24.79 (+7.92%)

- Taiwan Semiconductor Manufacturing (TSM): $245.60, +$8.04 (+3.38%)

These companies beat earnings expectations and traded higher following their reports.

Interestingly, stock futures were mostly flat after these upbeat earnings, but the mood shifted after the 8:30 AM ET release of retail sales and jobless claims data, which triggered a strong open and sustained gains throughout the session.

Retail sales in June rose by 0.6% month-over-month after two consecutive monthly declines. Initial jobless claims for the previous week fell by 7,000 to 221,000.

The increase in retail sales and the surprisingly low level of jobless claims sent a strong signal about consumer spending potential, which was reflected in the stock market's upward move.

Broad buying interest led to nine of eleven sectors closing in the green, with both the strength and breadth of the rally improving throughout the session.

The information technology sector (+0.9%) was among the leaders, with chipmakers rising after the Taiwan Semi report. The PHLX Semiconductor Index ended the session up 0.7%.

The rally in tech stocks helped the Nasdaq Composite (+0.7%) reach a new all-time high of 20,911.83. Big tech wasn't the only winner — demand for risk assets lifted all parts of the market.

Small-cap stocks outperformed the broader market, with the Russell 2000 gaining 1.2%. Mid-cap stocks followed a similar trend, as the S&P MidCap 400 rose 1.1%.

Large-cap stocks didn't underperform, but small caps simply did better, helped by growing optimism about economic expansion.

The Vanguard Mega Cap Growth ETF closed up 0.6%, slightly outperforming the S&P 500's +0.5%.

The Treasury market was subdued by positive economic data and comments from New York Fed President John Williams and Fed Governor Lisa Cook, both FOMC voting members. They noted that the current interest rate is appropriate for present conditions, including potential tariff-driven inflation in the coming months.

Treasuries saw modest losses, with short-term bonds underperforming long-term ones as the yield curve flattened:

- The 2-year yield rose 3 basis points to 3.92%

- The 10-year yield rose 1 basis point to 4.47%

- The US dollar index rose 0.3% to 98.68

Year-to-date performance:

- Nasdaq Composite: +8.15%

- S&P 500: +7.1%

- Dow Jones Industrial Average: +4.6%

- S&P MidCap 400: +1.7%

- Russell 2000: +1.1%

Economic calendar

Retail sales (June): +0.6% MoM (consensus: +0.2%) after a -0.9% decline in May

Retail sales ex-autos: +0.5% MoM (consensus: +0.3%) after an upward revision to -0.2% from -0.3%

Key takeaway: Sales growth was broad-based after weakness in April and May. June data showed rising discretionary spending in:

Autos: +1.2%

Clothing: +0.9%

Building materials and garden supplies: +0.9%

Food services and bars: +0.6%

Initial jobless claims for the week ending July 12: 221,000 (consensus: 230,000)

Continuing claims for the week ending July 5: 1.956 million (+2,000)

Takeaway The surprisingly low level of initial claims signals limited layoffs, supporting favorable business conditions and economic outlook.

Other economic data

Philadelphia Fed Index (July): 15.9 (consensus: -0.2, previous: -4.0), driven by gains in new orders, shipments, and employment — though prices paid and received also rose.

Import prices (June): +0.1% overall

Export prices (June): +0.5% MoM

YoY:

Import prices: -0.2%

Non-fuel imports: +1.2%

Export prices: +2.8%

Non-ag exports: +2.9%

NAHB Housing Market Index (July): 33 (vs. 32 forecast, unchanged from June)

Business Inventories (May): 0.0% (vs. -0.1% forecast, same as prior)

Energy market Brent crude is now trading at $70.10. Oil is once again testing the $70 mark, supported by US market strength.

Conclusion

After spending a long time below the 6,300 level, optimism has taken over the US market, and a new rally is underway. Stay long and keep watching.